Sending employees on assignments abroad can be an expensive endeavour, however, companies can structure their assignments in various ways to ensure they are more cost effective. One of the key considerations in structuring international assignments is the tax implications and benefits in host countries.

In this article we look at international assignments and taxation from a French perspective, exploring the French income tax landscape in comparison with the rest of Europe first and then touching on the factors employers need to be mindful of when sending employees overseas.

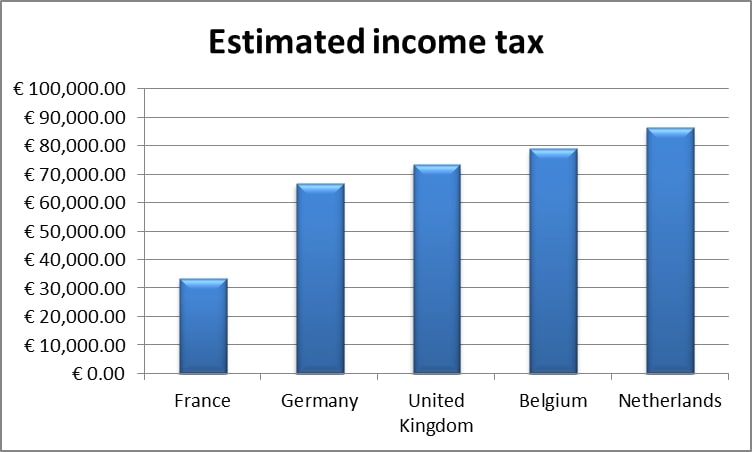

INCOME TAX COMPARISON: FRANCE VS REST OF EUROPE

It remains a popular belief that French employees assigned in a foreign country will pay less income tax abroad than in France. However, taking into account the French personal income tax regime, it is evident that the taxation of professional income in France may actually be more favourable than other foreign systems.

For example, what would the income tax be in various host countries for a married couple with two children and a global taxable income of EUR 200,000?

INTERNATIONAL ASSIGNMENTS AND TAXATION

It is important that the tax impacts of an international assignment not be neglected, and although some companies may consider this a private matter, employers who send employees abroad must at least, within the scope of its information obligation, draw the employee’s attention to their tax situation once abroad. The employer’s implication may also include tax equalization or a comparative study of the employee’s net income after social charges and tax during the assignment.

Tax equalization: Considerations

Tax equalization ensures an employee only pays an amount of theoretical tax, while on assignment, equivalent to what they would have paid should they have remained in the host country. On the other hand, the employer pays the actual amount of tax due in the host country. This practice, which is not governed by any specific regulation, must be clearly agreed between the employer and employee before work abroad commences.

In order to guarantee a net income (after social charges and tax income) equal to what the employee would receive in the host country, both parties must clearly define:

- The reference salary used to calculate the “theoretical” personal income tax: should it be the pre expatriation salary, or the base salary during the assignment, which generally takes into account an “upgrade” linked to the mobility?

- The family status of the employee and the other income: on which basis should personal income tax be computed? Will non-professional income of the household be included?

- Other compensation items such as variable compensation, equity based schemes, deferred compensation, profit sharing schemes, etc.: should they be taken into account?

Although there is no clear guideline, generally only professional income of the employee will be taken into account for tax equalization, along with the employee’s full family ratio so that the exclusion of the household’s other income would be partly compensated (the theoretical personal income tax being lower, and the net guaranteed income higher).

The other compensation items are generally treated separately as it requires an analysis of the tax and social security treatment of these items in the host country. With respect to Employee share schemes, for example, employers will need to determine:

- Whether a taxable event occurs in the host country,

- If the host country applies the OECD principles in relation to the sharing of the right to tax the acquisition gain, and

- How the acquisition gain is taxed.

Specific attention must also be given to the means of “payment” of certain compensation items. Housing may generally be a rather easy way to optimize the tax and social security treatment of the tax benefit, particularly in countries where housing costs are extremely high. The tax impact of the provision of the flat/house by the employer (which would be the owner of the lessor) is in many countries far more limited than the one of a mere refund of the rent. In Japan and Hong Kong for example, where the housing costs are particularly high, the benefit in kind is taxable only up to 5% of the actual rent and to 10% of the taxable income respectively.

Expatriate tax breaks

Similar to the “inbound” expatriates’ regime implemented by France since 2005, and regularly loosened since that date, various countries allow talented workers from abroad to benefit from tax breaks. Subject to meeting certain conditions, employees can benefit from tax rebate on their taxable income in European countries which include Belgium (Foreign executives regime), the Netherlands (30% ruling), both recently amended, the United Kingdom (Remittance Basis), Denmark, and Italy . Some non-European countries also have tax breaks for expatriates, such as China.